The Biggest Insurance Risks Facing Pizzerias in New York What Every Pizzeria Owner Should Understand About Protecting Their Business

Penny Hendrie

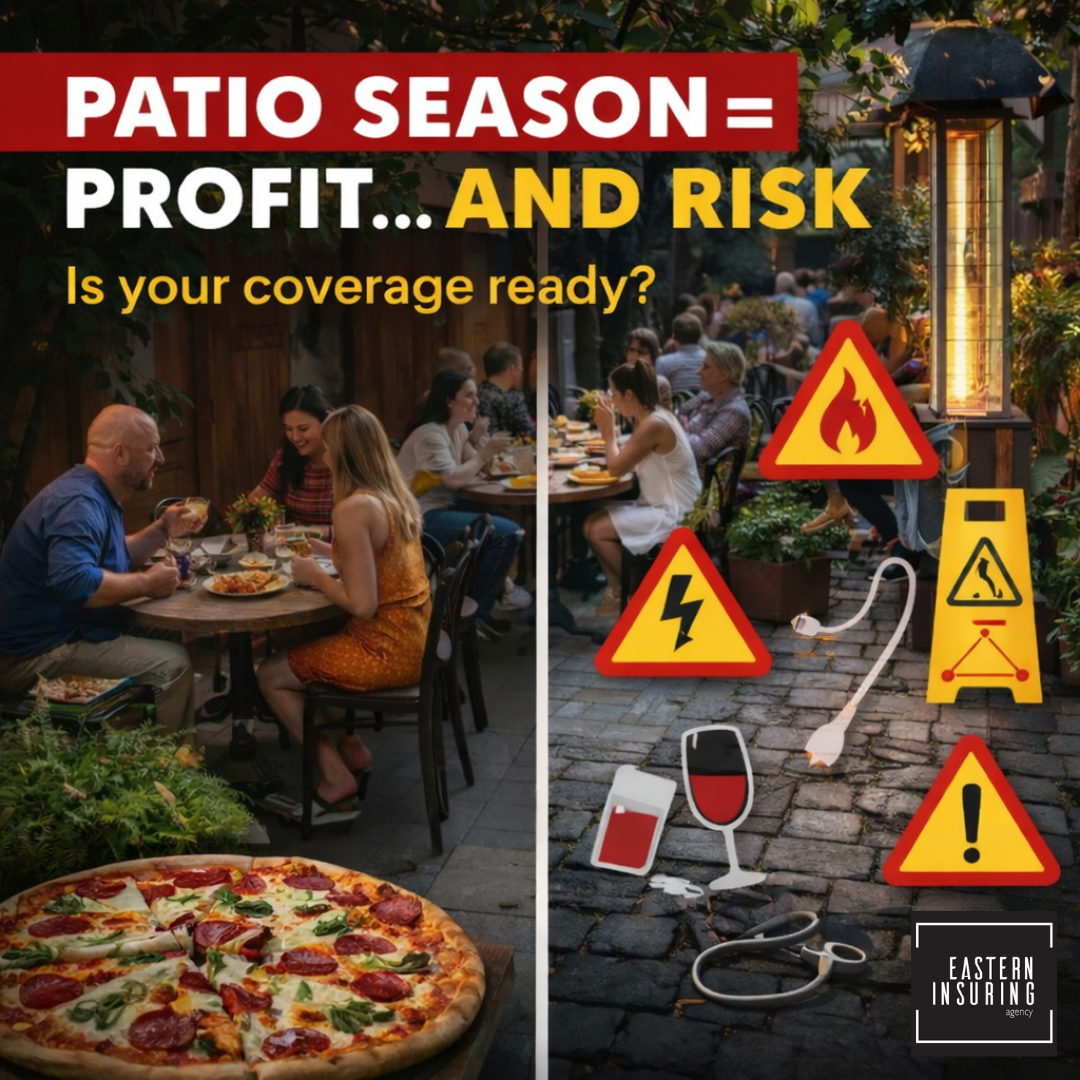

Running a pizzeria is about more than making great pizza.

Owners manage employees, equipment, delivery operations, customer safety, and food handling every single day. While many of these challenges are simply part of the business, they also create exposures that can lead to costly insurance claims if they are not properly addressed.

From my experience working with restaurants across New York, several risks consistently appear in pizzerias. Understanding these exposures—and planning for them—can help protect both your operations and your long-term profitability.

From my experience working with restaurants across New York, several risks consistently appear in pizzerias. Understanding these exposures—and planning for them—can help protect both your operations and your long-term profitability.

Below are some of the most common insurance risks facing pizzerias today.

Slip-and-Fall Accidents

Slip-and-fall accidents are among the most common liability claims in restaurants.

Pizzerias are particularly vulnerable because of the environment. Grease, spilled drinks, wet floors, and heavy foot traffic create natural hazards for both employees and customers.

Common causes of slip-and-fall incidents include:

Wet floors from spills or mopping floors from spills or mopping

Rain or snow tracked in from outside

Grease buildup in kitchen areas

Uneven flooring or worn mats

Even minor accidents can lead to medical costs and potential liability claims. Preventative steps such as non-slip flooring, prompt spill cleanup, proper signage, and regular floor inspections can significantly reduce these risks.

From an insurance standpoint, having strong liability coverage and documented safety procedures is essential.

Workers’ Compensation Claims

Restaurants have some of the most physically demanding work environments. In pizzerias, employees regularly lift heavy ingredient bags, operate hot ovens, carry trays of food, and work quickly in tight spaces.

Some of the most common workers’ compensation claims include:

Slips and trips in the kitchen

Burns from ovens or hot equipment

Lifting injuries from flour or ingredient bags

Repetitive strain injuries from food preparation

These types of injuries can result in medical costs, lost wages, and increased insurance premiums. Implementing strong safety practices—such as employee training, proper lifting techniques, and organized workspaces—can help reduce the likelihood of these claims.

Equipment Breakdown

Pizzerias depend heavily on specialized equipment. Pizza ovens, refrigeration systems, dough mixers, exhaust systems, and HVAC units often operate long hours and under significant demand.

When this equipment fails, the impact can be immediate.

Equipment breakdown can lead to:

Lost revenue during downtime

Spoiled food inventory

Expensive emergency repairs

Customer service disruptions

Many restaurant owners are surprised to learn that a standard property policy may not automatically cover mechanical breakdowns. Equipment breakdown coverage can help fill that gap and protect against losses caused by sudden mechanical or electrical failure.

Food Contamination and Food Safety Risks

Food safety is critical in any restaurant, and pizzerias are no exception.

Contamination can occur in several ways, including:

Improper food storage temperatures

Cross-contamination during preparation

Equipment malfunction affecting refrigeration

Pests or environmental contamination

If customers become ill from contaminated food, the financial consequences can include medical claims, legal expenses, and reputational damage. In severe cases, restaurants may also face temporary closure by health authorities.

Maintaining strict food safety procedures, regular inspections, and proper staff training are essential risk management steps. Insurance policies can also provide protection against certain food-related liability exposures.

Delivery-Related Exposures

Delivery has become an important revenue stream for many pizzerias. However, it introduces new risks that many owners overlook.

Delivery exposures can include:

Auto accidents involving delivery drivers

Injuries during deliveries

Damage to vehicles or property

Liability claims resulting from accidents

If employees use their own vehicles for delivery, there may be gaps between personal auto insurance and business liability. In many cases, restaurants may need additional protection such as hired and non-owned auto coverage.

Understanding how delivery operations affect insurance coverage is an important step for any pizzeria offering this service.

Property Damage

Property losses are another major risk for pizzerias.

Restaurants face exposure to events such as:

Kitchen fires

Electrical issues

Storm damage

Water damage from plumbing failures

Because pizzerias rely on specialized equipment and kitchen infrastructure, property damage can lead to significant repair costs and business interruption.

Proper property insurance coverage, along with preventive maintenance and fire protection systems, can help reduce the financial impact of these events.

Why Pizzerias Need Specialized Insurance Advice

While many businesses carry general commercial insurance, restaurants—and pizzerias in particular—have unique operational risks that require careful attention.

Between kitchen equipment, delivery operations, food safety responsibilities, and customer traffic, pizzerias face a combination of exposures that are very different from other businesses.

Working with an insurance advisor who understands the restaurant industry can help ensure that coverage aligns with how your business actually operates. A thoughtful approach to risk management and insurance planning allows owners to focus on what they do best: serving their customers and growing their business.

Recent posts

Liquor store insurance in New York explained. Learn about theft, liability, and inventory risks—and how to better protect your business.

Opening your pool in New York? Learn how insurance applies to pools, liability risks, safety requirements, and what to review before the season starts.

Convenience store insurance in New York explained. Learn about theft, liability, and underwriting risks—and how to better protect your business.

New York storm season is here. Learn what homeowners insurance may not cover—flood, sewer backup, and wind damage—and why a review matters.

Own a boat, motorcycle, or ATV in New York? Learn how insurance coverage works, where gaps may exist, and why a policy review matters.

Apartment building insurance in New York explained. Learn what impacts renewals, from water damage to maintenance—and how to better position your property.

Antique store insurance in New York explained. Learn about valuation, theft risks, and coverage considerations for high-value inventory.

Florist insurance in New York explained. Learn key risks like spoilage, delivery liability, and event exposure—and how to better protect your business.

Planning a home project in New York? Learn how homeowners insurance applies to renovations, liability, and materials—and where gaps may exist.

Strong safety programs help restaurants reduce injuries, prevent claims, and lower insurance costs—protecting staff, customers, and profits.