How Insurance Helps Contractors Win More Jobs

Penny Hendrie

Many contractors think of insurance as simply another business expense—something required to stay compliant or satisfy basic jobsite requirements. But in today’s construction environment, insurance plays a much larger role.

For many artisan contractors, having the right insurance program can actually help them win more work.

For many artisan contractors, having the right insurance program can actually help them win more work.

General contractors, project owners, property managers, and municipalities increasingly rely on insurance documentation to determine which subcontractors they are willing to work with. Contractors who maintain the proper coverage, documentation, and limits are often in a stronger position to secure projects and build long-term business relationships.

Insurance is not just protection—it is also a signal of professionalism and reliability.

Why General Contractors Require Insurance

Construction projects involve many moving parts. A general contractor may oversee electricians, plumbers, carpenters, drywall installers, flooring specialists, painters, and HVAC technicians all working on the same jobsite.

With multiple contractors involved, the potential for accidents or property damage increases.

To manage that risk, general contractors often require subcontractors to maintain specific insurance coverage before they are allowed to begin work. This helps ensure that if a problem occurs, the responsible party has the financial resources to address it.

Most general contractors require subcontractors to provide a Certificate of Insurance (COI)

before work begins. This document verifies that the subcontractor carries the appropriate insurance policies and coverage limits.

Without this documentation, many contractors will not be permitted to work on the project.

Common Insurance Requirements for Contractors

Contractors may encounter a variety of insurance requirements when bidding or accepting new projects.

These requirements often include:

General Liability Insurance

General liability policies protect against property damage and bodily injury claims caused by the contractor’s work. Most project owners require contractors to carry at least $1 million in general liability coverage.

Workers Compensation Insurance

If a contractor has employees, workers compensation insurance is often required to ensure that workplace injuries are covered.

Commercial Auto Insurance

Contractors who bring vehicles onto a jobsite may also be required to maintain commercial auto liability coverage.

In addition to these policies, contractors are often asked to provide specific endorsements that modify their coverage.

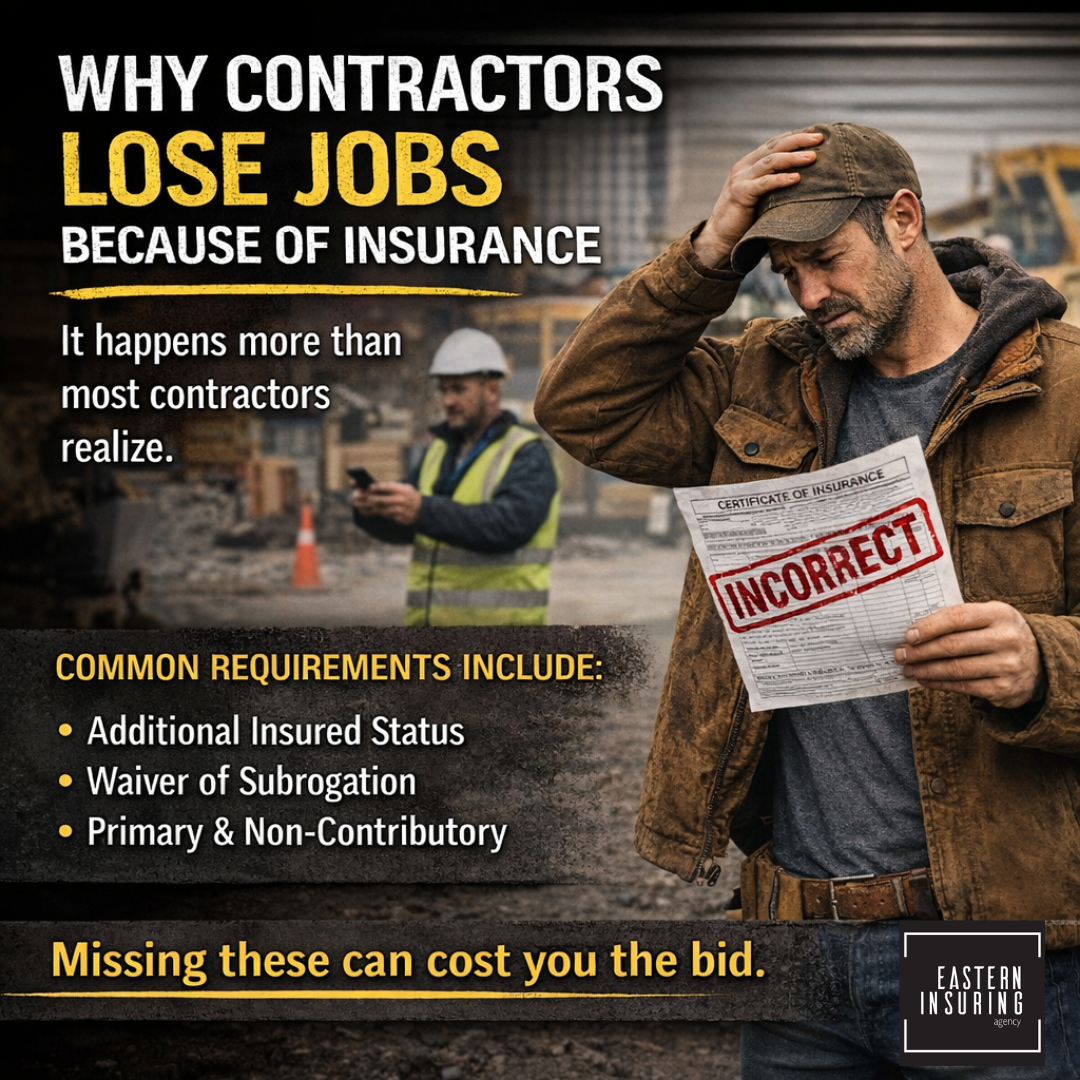

Understanding Additional Insured Requirements

One of the most common requests contractors receive involves adding another party as an Additional Insured on their general liability policy.

This endorsement extends liability protection to another party—typically the general contractor or project owner—for claims that arise from the subcontractor’s work.

For example, if a subcontractor’s work causes property damage and the homeowner sues both the subcontractor and the general contractor, the additional insured endorsement may help provide protection for both parties.

While these endorsements are common in construction contracts, they must be added correctly to the policy in order to meet the contract requirements.

Contractors who work with experienced insurance advisors can ensure these endorsements are handled properly.

The Importance of Quick Certificates of Insurance

Speed matters in the construction industry.

General contractors often request certificates of insurance on short notice, particularly when a project is about to begin. Contractors who cannot provide documentation quickly may find themselves losing opportunities.

This is why many contractors work with insurance agencies that can provide fast certificate turnaround.

Being able to produce a certificate of insurance the same day—or even within minutes—can make a significant difference when competing for projects.

Insurance Limits Can Affect Project Opportunities

As contractors grow, they often pursue larger and more complex projects. These opportunities frequently come with higher insurance requirements.

For example, a contractor working on small residential projects may carry a $1 million liability policy. However, a larger commercial project may require:

• $2 million in general liability coverage

• Umbrella liability insurance

• Additional insured endorsements

Contractors who prepare their insurance program in advance can position themselves to pursue larger opportunities as they arise.

Without adequate limits in place, a contractor may be forced to decline projects that would otherwise help the business grow.

Insurance Demonstrates Professionalism

Contractors who maintain strong insurance coverage send an important message to clients and project partners.

It shows that they:

• Take their business seriously

• Understand the risks of construction work

• Are prepared to handle unexpected events

Homeowners and project managers are more comfortable hiring contractors who demonstrate this level of professionalism.

In many cases, insurance coverage helps build trust before the project even begins.

Turning Insurance Into a Competitive Advantage

When contractors understand how insurance fits into the construction industry, they can begin to view it as more than just a requirement.

Proper coverage allows contractors to:

• Meet project requirements quickly

• Build trust with general contractors and clients

• Pursue larger and more complex jobs

• Protect their business from unexpected claims

In other words, the right insurance program supports both protection and growth.

The Role of a Construction-Focused Insurance Advisor

Because construction contracts and insurance requirements can be complex, many contractors benefit from working with an insurance advisor who understands the unique needs of the trades.

An experienced advisor can help contractors:

• Review contract insurance requirements

• Ensure policies meet project standards

• Provide certificates of insurance quickly

• Identify coverage gaps before problems occur

For artisan contractors focused on building a successful business, the right insurance partner can help turn risk management into a strategic advantage.

When contractors combine skilled workmanship with the proper protection, they position themselves for long-term success in an increasingly competitive industry.

Recent posts

Liquor store insurance in New York explained. Learn about theft, liability, and inventory risks—and how to better protect your business.

Opening your pool in New York? Learn how insurance applies to pools, liability risks, safety requirements, and what to review before the season starts.

Convenience store insurance in New York explained. Learn about theft, liability, and underwriting risks—and how to better protect your business.

New York storm season is here. Learn what homeowners insurance may not cover—flood, sewer backup, and wind damage—and why a review matters.

Own a boat, motorcycle, or ATV in New York? Learn how insurance coverage works, where gaps may exist, and why a policy review matters.

Apartment building insurance in New York explained. Learn what impacts renewals, from water damage to maintenance—and how to better position your property.

Antique store insurance in New York explained. Learn about valuation, theft risks, and coverage considerations for high-value inventory.

Florist insurance in New York explained. Learn key risks like spoilage, delivery liability, and event exposure—and how to better protect your business.

Planning a home project in New York? Learn how homeowners insurance applies to renovations, liability, and materials—and where gaps may exist.

Strong safety programs help restaurants reduce injuries, prevent claims, and lower insurance costs—protecting staff, customers, and profits.